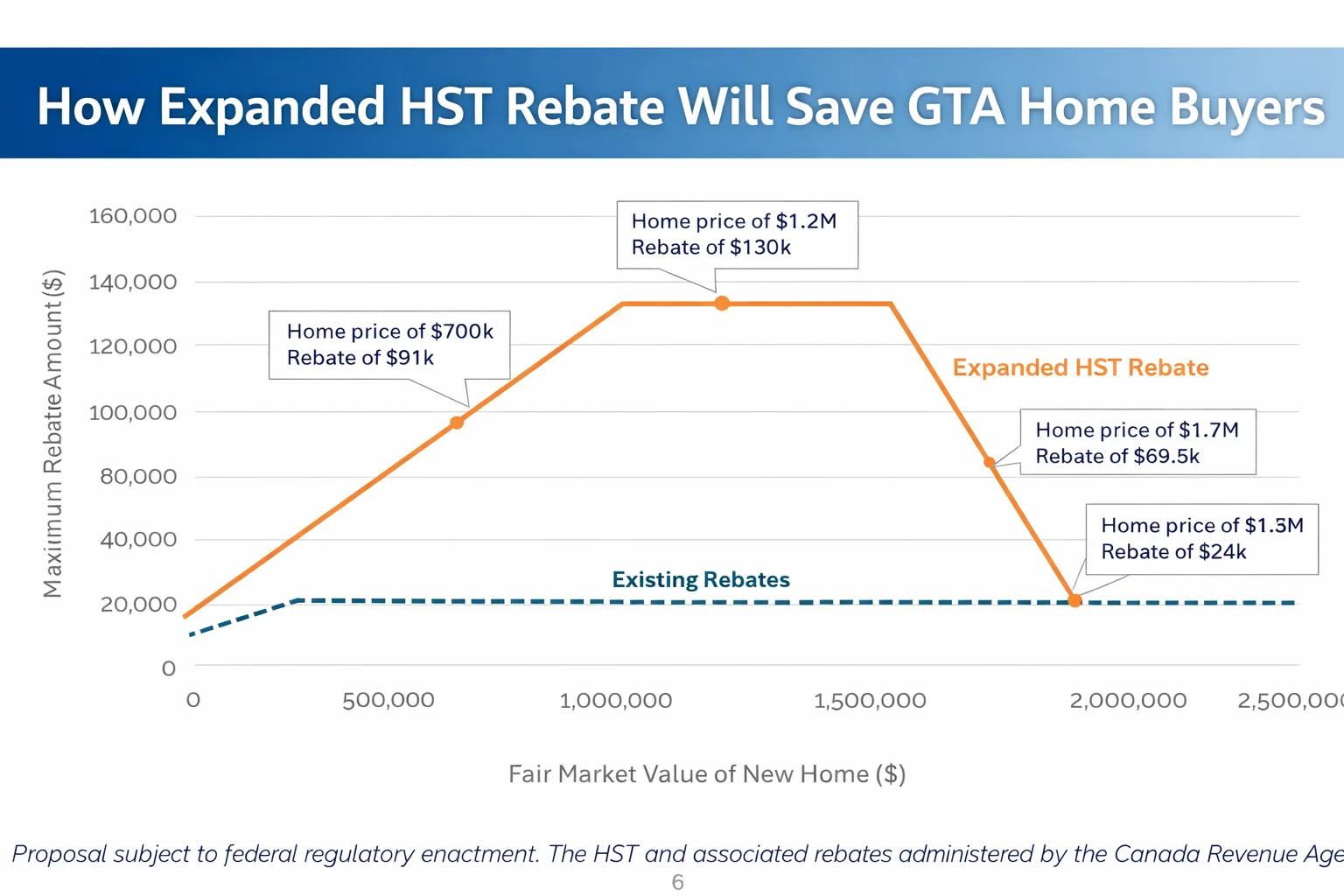

First-Time Home Buyer's Mortgage Guide for the GTA

Navigating the mortgage landscape as a first-time buyer in the Greater Toronto Area can feel overwhelming. With home prices in Toronto, Brampton, Mississauga, and Vaughan among the highest in Canada, understanding the latest rules, securing the best rate, and maximizing every government incentive is critical.

This guide breaks down everything you need to know to confidently finance your first home in the GTA in 2026.

The Game-Changing 2024-2026 Mortgage Rule Reforms

The federal government introduced the boldest mortgage reforms in decades, effective December 15, 2024. These changes are still in effect in 2026 and represent a massive win for first-time buyers in the GTA:

1. Insured Mortgage Price Cap Raised to $1.5 Million

The maximum purchase price for an insured (high-ratio) mortgage was raised from $1 million to $1.5 million. This is a game-changer for GTA buyers where the average home price regularly exceeds $1 million.

2. 30-Year Amortization for All First-Time Buyers

First-time buyers can now choose a 30-year amortization instead of the traditional 25 years, regardless of property type.

3. Stress Test Changes for Lender Switches

If you have an insured mortgage and want to switch lenders at renewal, the mortgage stress test no longer applies — as long as your loan amount and amortization remain unchanged. This gives you more bargaining power at renewal time.

Understanding Down Payment Rules in 2026

The minimum down payment in Canada follows a tiered structure:

Down Payment Examples for GTA Cities

The Mortgage Stress Test Explained

Every buyer in Canada must pass the mortgage stress test, which ensures you can afford payments at a higher rate than your actual contract rate.

The stress test is the same for fixed and variable rate mortgages. Working with an experienced mortgage broker can help you maximize your qualifying amount.

Current Mortgage Rates in Canada (2026)

Rates fluctuate, but here is a snapshot of what major Canadian banks are offering for insured 5-year fixed and variable mortgages:

5-Year Fixed Rates (Insured)

5-Year Variable Rates (Insured)

Bank of Canada Rate Outlook

The Bank of Canada overnight rate sits at 2.25% and is expected to remain stable through 2026. Most major bank economists forecast no further cuts this year, meaning current rates are likely near their floor for the cycle.

Pro Tip: Broker vs. Bank

Mortgage brokers consistently offer lower rates than the Big Five banks because they shop across 30+ lenders. For first-time buyers, this can save $10,000-$30,000 over the life of your mortgage. Always get at least 3 quotes before committing.

Fixed vs. Variable: Which Is Right for You?

Fixed Rate Mortgage

Variable Rate Mortgage

For most first-time buyers in the GTA in 2026, a 5-year fixed rate through a broker offers the best balance of security and savings.

CMHC Mortgage Insurance: What You Need to Know

If your down payment is less than 20%, you must pay mortgage default insurance through CMHC, Sagen, or Canada Guaranty.

Insurance Premium Rates

Example for a $900,000 Home in Brampton

The insurance premium is added to your mortgage, so you do not need to pay it upfront.

Step-by-Step: Your First Mortgage in the GTA

Step 1: Get Pre-Approved (Before You Start Looking)

A mortgage pre-approval locks in your rate for 90-120 days and tells you exactly how much you can afford.

Step 2: Maximize Your Down Payment

Combine multiple sources to build the largest down payment possible:

Step 3: Budget for Closing Costs

Many first-time buyers underestimate closing costs. In the GTA, budget 1.5% to 4% of the purchase price:

Step 4: Choose Your Mortgage Features

Step 5: Make Your Offer

Once you find your home, your real estate agent will help you draft a competitive offer. Include a financing condition (usually 5 business days) to finalize your mortgage.

Step 6: Finalize and Close

After your offer is accepted:

Smart Strategies for GTA First-Time Buyers

1. Consider Emerging GTA Neighbourhoods

While downtown Toronto commands premium prices, adjacent communities offer excellent value:

2. Look at New Construction

New builds offer several advantages for first-time buyers:

3. Explore Co-Ownership

Buying with a sibling, partner, or friend is increasingly common in the GTA. Both incomes count toward qualification, making it easier to enter the market.

4. Use a Mortgage Broker

Brokers negotiate on your behalf across dozens of lenders, often securing rates 0.3%-0.5% lower than what you would get walking into a bank branch.

Common Mistakes to Avoid

How Team Shailesh Can Help

Team Shailesh is a trusted name in GTA real estate. While we specialize in commercial real estate — business sales, pharmacy acquisitions, medical centre leases — we work closely with a network of top residential agents and mortgage professionals across Brampton, Mississauga, Toronto, Vaughan, Oakville, and Hamilton.

Whether you are buying your first home, exploring mixed-use investment properties, or planning your long-term real estate strategy, we can connect you with the right experts.

Contact Team Shailesh today for a free consultation. Call 647-877-7766 or visit teamshailesh.ca.

Related Articles

Top 10 High Schools in Ontario (2025-2026) – Rankings, EQAO Scores & Home Prices

Read more

First-Time Homebuyer Perks in Ontario, Canada: Complete 2026 Guide

Read more