First-Time Homebuyer Perks in Ontario, Canada

Buying your first home in Ontario is one of the biggest financial decisions you will ever make. The good news? Both the federal and provincial governments offer a generous lineup of incentives, tax credits, and savings programs designed to make homeownership more accessible. If you are planning to buy in the Greater Toronto Area — including Brampton, Mississauga, Toronto, Vaughan, or Oakville — here is every perk you should know about in 2026.

1. First Home Savings Account (FHSA)

The FHSA is one of the most powerful tools for first-time buyers in Canada. Introduced in 2023, it combines the best features of an RRSP and a TFSA:

This is especially valuable for buyers saving toward a down payment on a property in the GTA, where average home prices remain among the highest in Canada.

2. Home Buyers Plan (HBP)

The Home Buyers Plan allows you to withdraw up to $60,000 from your RRSP tax-free to buy or build your first home ($120,000 per couple).

Pro Tip for GTA Buyers

With average home prices in Toronto exceeding $1 million and Brampton and Mississauga averaging $900,000+, combining your FHSA ($40,000) with the HBP ($60,000 per person) can give you up to $100,000 in tax-advantaged down payment savings — or $200,000 as a couple.

3. Ontario Land Transfer Tax Refund

Ontario charges a land transfer tax on every property purchase. First-time buyers can claim a refund of up to $4,000, which covers the full tax on homes priced up to $368,000.

For homes above $368,000 (which is most properties in the GTA), you still save $4,000 off the total land transfer tax owing.

4. Toronto Municipal Land Transfer Tax Refund

If you are buying within the City of Toronto, you face a second land transfer tax — the Municipal Land Transfer Tax (MLTT). First-time buyers can claim a refund of up to $4,475.

This is one reason many first-time buyers in the GTA consider communities like Brampton, Mississauga, or Hamilton — you avoid the extra municipal tax entirely.

5. Home Buyers Tax Credit (HBTC)

The federal Home Buyers Tax Credit provides a $10,000 non-refundable tax credit, resulting in up to $1,500 in tax savings.

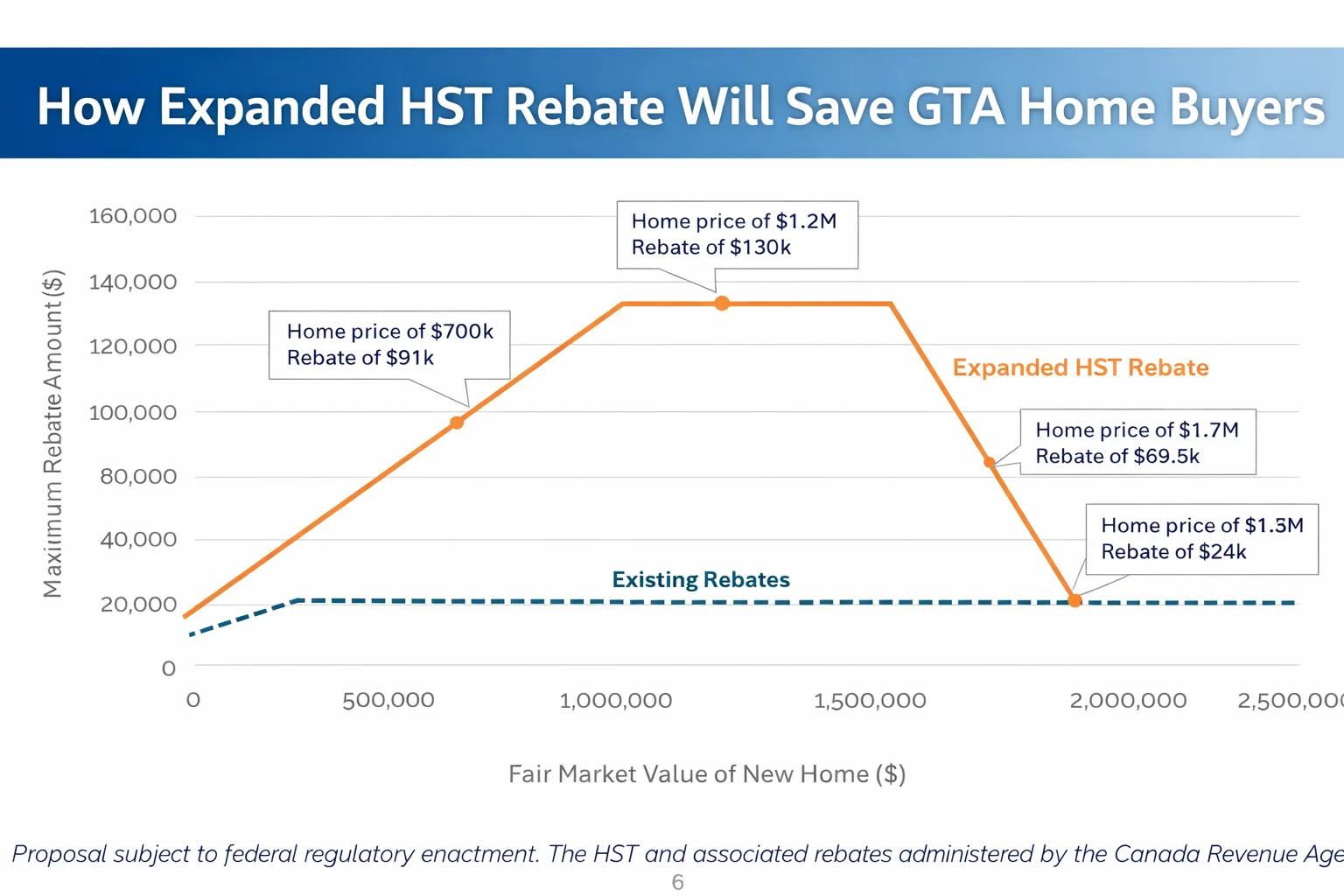

6. GST/HST New Housing Rebate

If you are buying a newly built home in Ontario, you may be eligible for a rebate on the HST paid:

This is a significant incentive for buyers considering new construction in growing GTA communities like Brampton, Vaughan, and Milton where new developments are abundant.

7. First-Time Home Buyer Incentive (Shared Equity)

The federal government offers a shared equity mortgage through the First-Time Home Buyer Incentive:

8. 30-Year Amortization on Insured Mortgages

💰 Lower monthly payments, more buying power

As of December 2024, first-time home buyers in Canada can access a 30-year amortization period on insured mortgages (those with a down payment under 20%). Previously, insured mortgages were capped at 25 years. This extra 5 years meaningfully reduces your monthly payment, making it easier to qualify for a mortgage and manage cash flow in those early ownership years.

Applies to: Buyers with less than 20% down payment who require CMHC mortgage insurance

Benefit: Reduces monthly payments vs. a 25-year amortization — can be hundreds of dollars per month lower on a GTA-area purchase

Trade-off: You pay more total interest over the life of the mortgage — consider paying extra on your mortgage when you can afford to

9. Additional Programs and Tips

CMHC Mortgage Insurance Discounts

Energy Efficiency Programs

Property Tax Programs

How Much Can You Save? A GTA Example

Let us say you are a first-time buyer purchasing a $750,000 resale home in Brampton:

For a $750,000 new build in Vaughan, add the HST rebate for potentially $50,000+ in total savings.

How Team Shailesh Can Help

While Team Shailesh specializes in commercial real estate, we understand the residential market through our network of trusted partners. Whether you are a first-time homebuyer looking for guidance, or an investor exploring both residential and commercial opportunities in the GTA, our team can connect you with the right professionals.

We also help first-time buyers who are interested in mixed-use properties — buildings with both residential and commercial components — which can be an excellent way to build wealth while living in your investment.

Contact Team Shailesh today for a free consultation about real estate opportunities across the Greater Toronto Area — Brampton, Mississauga, Toronto, Vaughan, Oakville, and Hamilton.

Related Articles

Top 10 High Schools in Ontario (2025-2026) – Rankings, EQAO Scores & Home Prices

Read more

First-Time Home Buyer's Mortgage Guide for the GTA: Rates, Rules & Expert Tips for 2026

Read more